In Your Face, Yet Under the Investment Radar

Here is a long but well worth the read post by Hoya Capital Real Estate. Thanks to Hoya Capital for permission to republish.

It has critically relevant facts and great graphics with strong analysis of Lamar and OUTFRONT. It includes OOH Industry comparisons with Clear Channel, other media and other REIT’s. I would suggest a must read to become more intimate with the the investment industries’ view of OOH. Billboard REITs: In Your Face, But Under the Radar

REIT Rankings: Billboards

(Hoya Capital, Co-Produced with Brad Thomas through iREIT on Alpha)

Billboard REIT Sector Overview

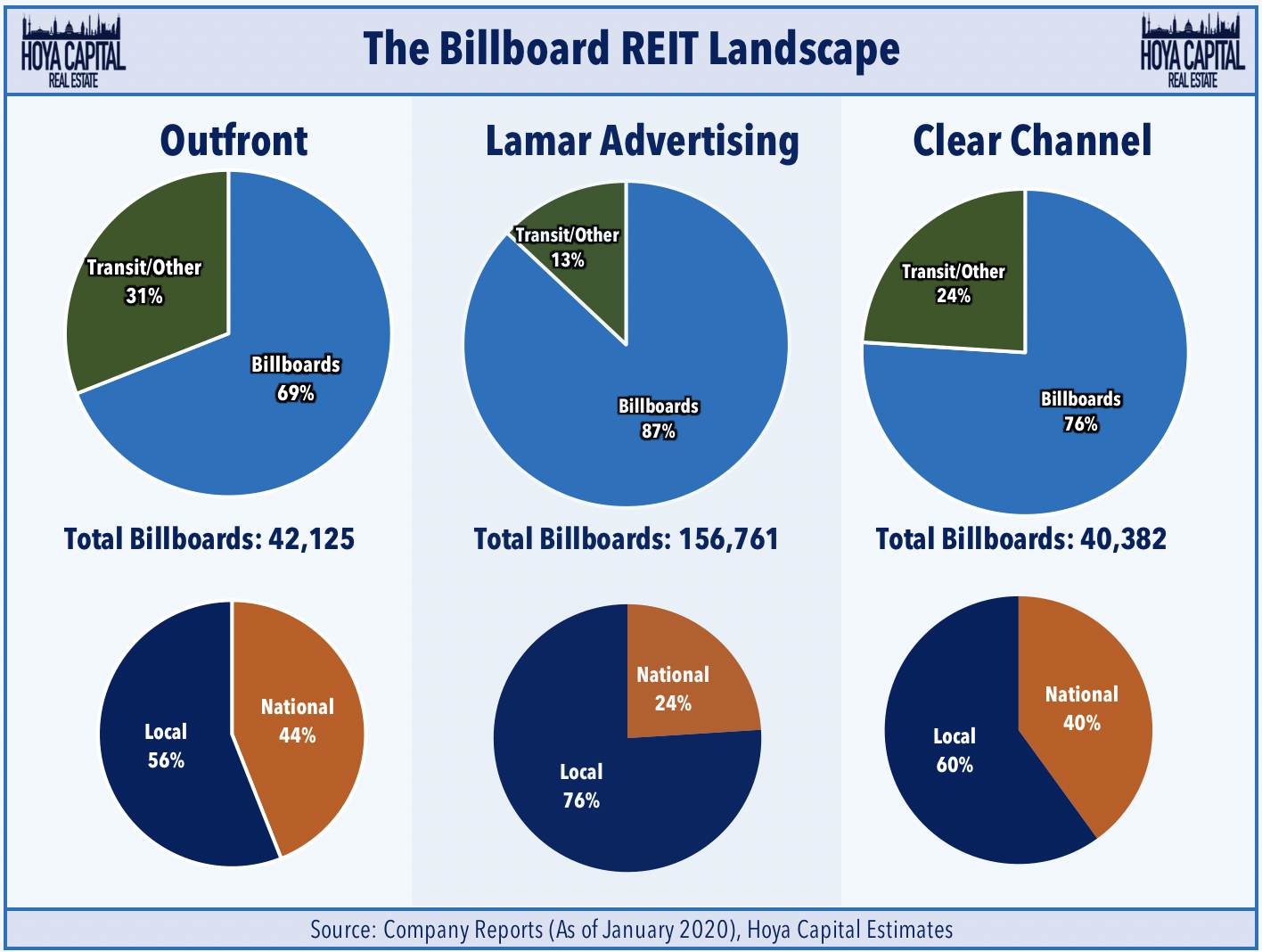

Emerging in the mid-2010s during the relatively short-lived ‘REIT Conversion Craze,’ we’re excited to launch coverage on one of the newest REIT sectors. In the Hoya Capital Billboard REIT Index, we track the two billboard REITs, which account for roughly $13 billion in market value: Lamar Advertising (LAMR) and Outfront Media (OUT) which combine to control roughly half of all advertising billboards in the United States. We also track non-REIT Clear Channel Outdoor (CCO), which is the third-largest billboard operator. A growth-oriented sector that pays a healthy dividend yield, Billboard REITs comprise roughly 1% of the broad-based commercial Real Estate ETF (VNQ).

Billboard REITs are the largest players in the “Out-of-Home” (OHH) advertising market, which includes not only billboards but also transit displays and other static and digital signage designed to reach consumers while they’re on the go. Outfront emerged in 2014 from a spin-off from CBS Outdoor, converting to a REIT soon thereafter while Lamar Advertising went public in 1996 and converted to a REIT in 2014. Clear Channel, meanwhile, remains a corporation but has explored a REIT conversion at various points in the last half-decade.

These companies derive around 75% of their revenues from billboards and the rest through transit advertising and other signage. Lamar operates as the most “pure-play” billboard company of the three while Outfront has a large transit-oriented business, highlighted by the company’s massive transit deal with the Metropolitan Transportation Authority (MTA). As we’ll discuss in more detail, billboard REITs are an operationally-intensive business with the majority of revenues driven by local advertising sales.

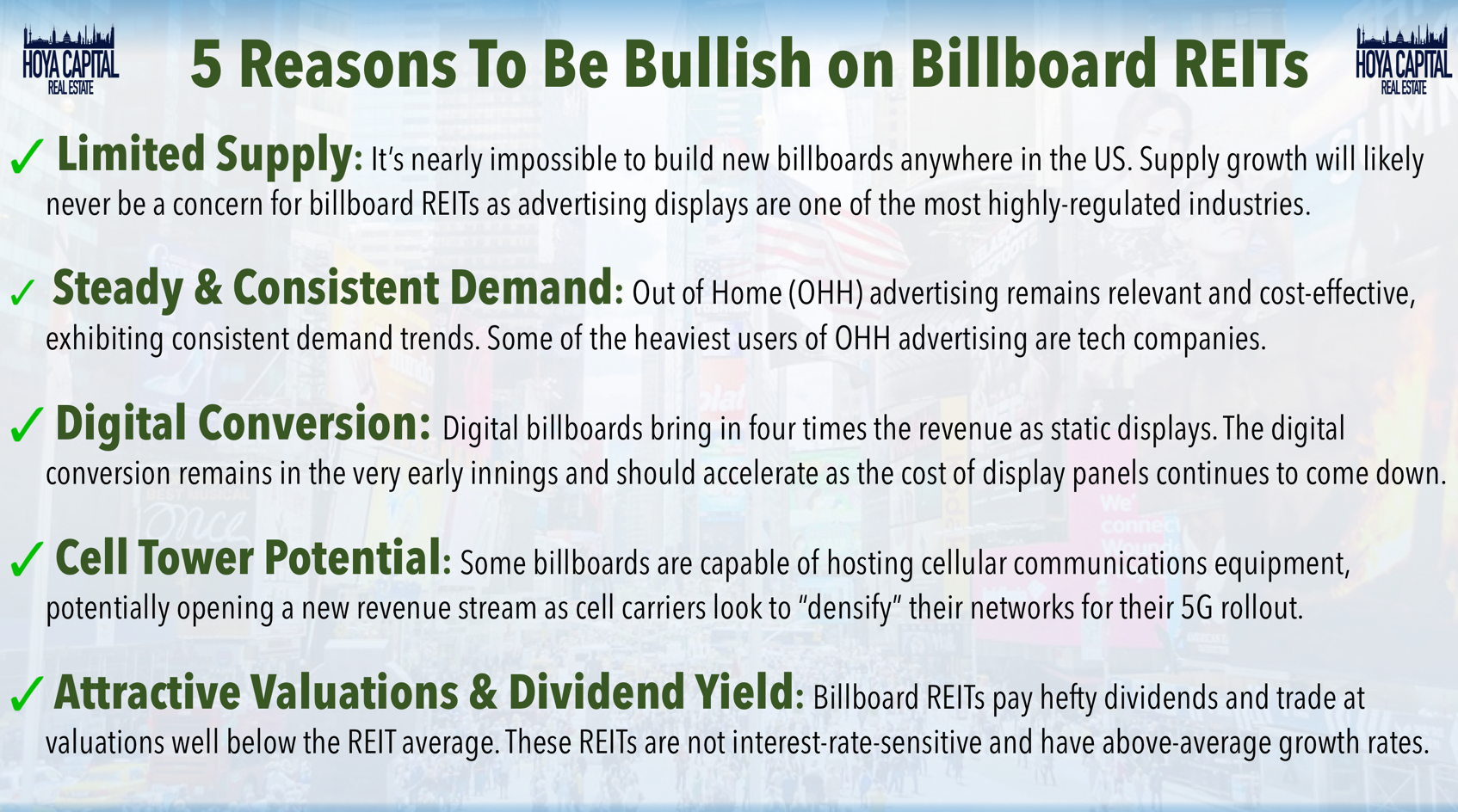

In the era of highly-personalized advertising and advanced tracking and ad-conversion metrics, OHH remains an attractive and cost-effective medium for mass-market and local advertisers as ads can’t be skipped, blocked, fast-forwarded, or consumed by “bots.” Spending on OHH advertising remains a small, but steadily growing segment of the advertising landscape. A report from PwC shows that spending on OHH is expected to rise roughly 3% per year through mid-2023, the second-strongest rate of growth behind internet advertising. These REITs are in the process of converting many of the highest-value locations from static billboards into digital display boards, which can bring in 2-4 times more revenue than typical static display boards.

Interestingly and somewhat ironically, some of the heaviest users of OHH advertising are technology companies including Apple (AAPL), T-Mobile (TMUS), Netflix (NFLX), and Facebook (FB) while television, retail, professional services, and restaurants are also heavy users. On a “cost-per-impression” or CPM basis, OHH advertising consistently ranks as the cheapest advertising medium and is especially effective for national mass-market brands and for local services (restaurants, gas stations) in the immediate proximity. A “top-heavy” industry, these three companies combine to control nearly two-thirds of all billboards and transit displays in the United States, but the remaining third is quite fragmented with thousands of individual landowners and permit-holders.

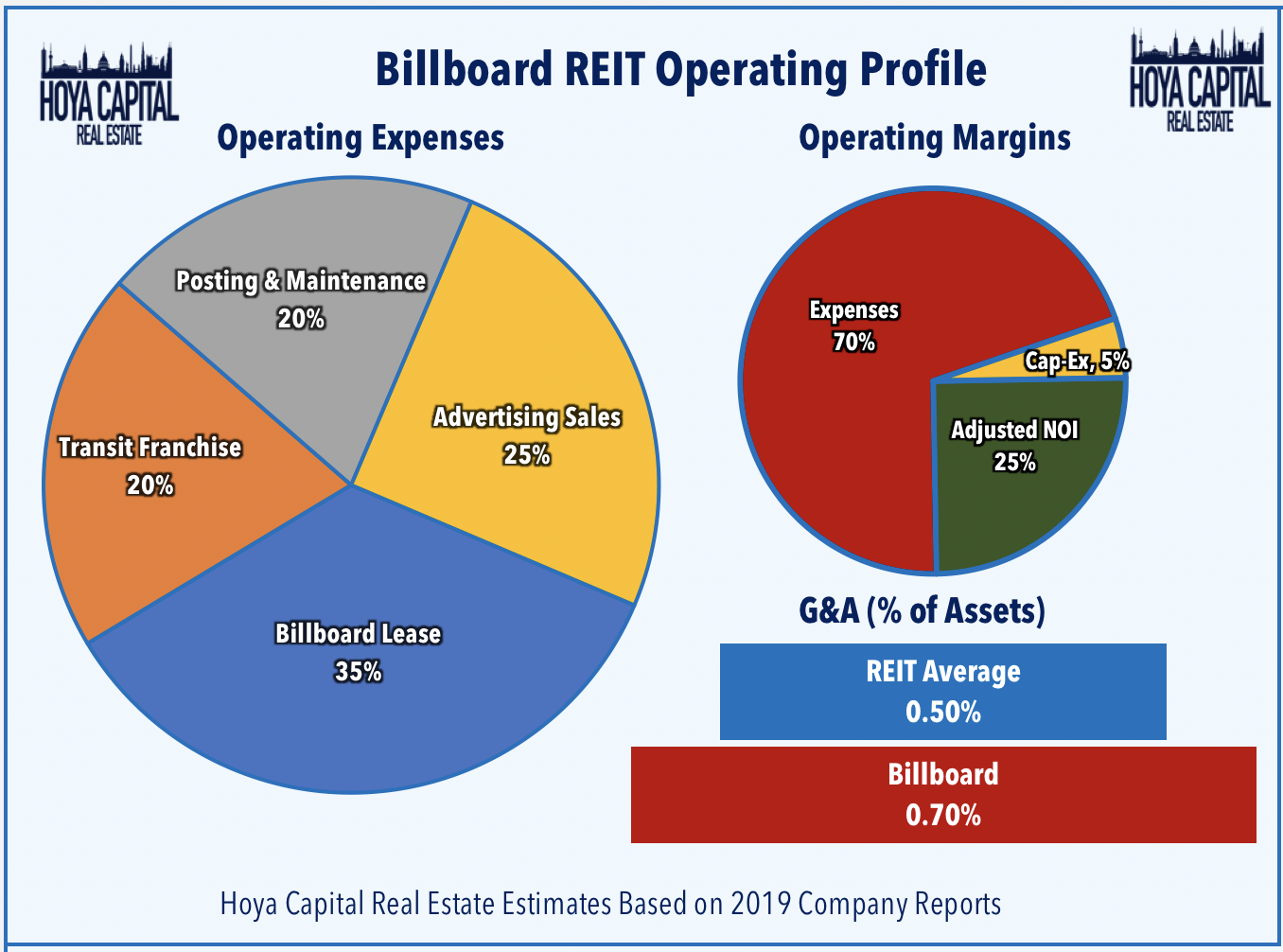

There are more than 300,000 billboards across the US, but don’t even think about trying to build any new ones. Signage remains one of the most highly-regulated industries ever since a 1965 law that limited new billboard construction along federal highways. The majority of existing billboards are “grandfathered-in” as “legal non-conforming” uses, which limits future supply growth but also makes it a challenge to upgrade or improve the displays. Some cities, for instance, require the removal of 2-3 existing billboards for every new digital upgrade. Sharing similar characteristics to the cell tower REIT industry (and in fact, many billboards host cellular equipment), billboard REITs own the display structure and the use-permit but not the land underneath, leasing it from thousands of individual landowners for terms of 5-15 years. Advertising contracts, meanwhile, typically run for 1-12 months and pricing is based on the billboard’s size, viewability, and impressions.

Unlike the cell tower REIT business, however, billboard management is a relatively low-margin and operationally-intensive business that requires a large advertising salesforce and fairly continual maintenance in the form of posting and maintaining static signage. Operating margins are below 30% compared to the 65-70% REIT sector average and these businesses operate with quite a bit of inherent operating leverage due to the long-term nature of their ground lease liabilities and the short-term nature of their advertising contracts. Capital expenditure needs, however, are relatively low at roughly 5% of revenues. The transition to digital may help to improve long-run operating margins but will result in elevated cap-ex as displays will need to be updated periodically with newer display technology to achieve the highest potential revenue.

Billboard REIT Stock Performance

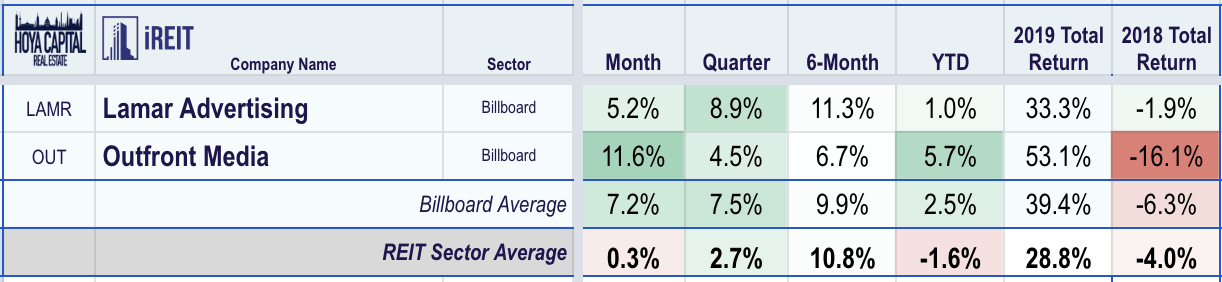

Billboard REITs delivered a stellar year in 2019, delivering total returns of nearly 40% compared to the 29% total returns from the broad-based REIT index and bouncing back from the 6% declines in 2018. The track record for each of these companies’ REIT conversions in 2014 has been a mixed bag, as Lamar has delivered steady outperformance while Outfront struggled from 2014 through 2018 before delivering strong performance in 2019. Lamar’s relatively conservative balance sheet and more pure-play focus on the higher-margin billboard business has been rewarded by investors while Outfront’s outsized exposure to transit advertising – specifically with the massive New York MTA deal – has been a continued source of concern for investors.

The script flipped in 2019 with Outfront surging more than 50%, outpacing the 33% total returns from Lamar. Outfront delivered a series of earnings beats, and through three quarters of results, is running ahead of its full-year AFFO growth guidance in the mid-single-digit range, driven by strong “same-board” organic revenue growth. Lamar has been no slouch either, expecting to end 2019 at the top-end of its AFFO guidance range. Both companies continue to make progress in their digital conversions with Outfront on pace for roughly 100 such conversions in 2019 and Lamar targeting 200. In future REIT Rankings updates on the billboard REIT sector, we will take a deeper dive into quarterly performance figures and underlying sector fundamentals.

Valuation of Billboard REITs

Despite their above-average 5-year FFO growth rate of roughly 5%, billboard REITs trade at discounted valuations relative to other REIT sectors based on consensus Free Cash Flow (aka AFFO, FAD, CAD) metrics. Powered by the iREIT Terminal, we show that billboard REITs trade at an estimated 15x Price to AFFO and trade at a modest 5% premium to Net Asset Value. We believe that maintaining a positive premium to NAV is especially critical for the billboard REIT sector, which will rely on equity capital raising to continue to fuel accretive external growth over the next decade through the combination of digital conversion upgrades and one-off and small portfolio acquisitions.

Billboard REITs Dividend Yield & Factor Sensitivity

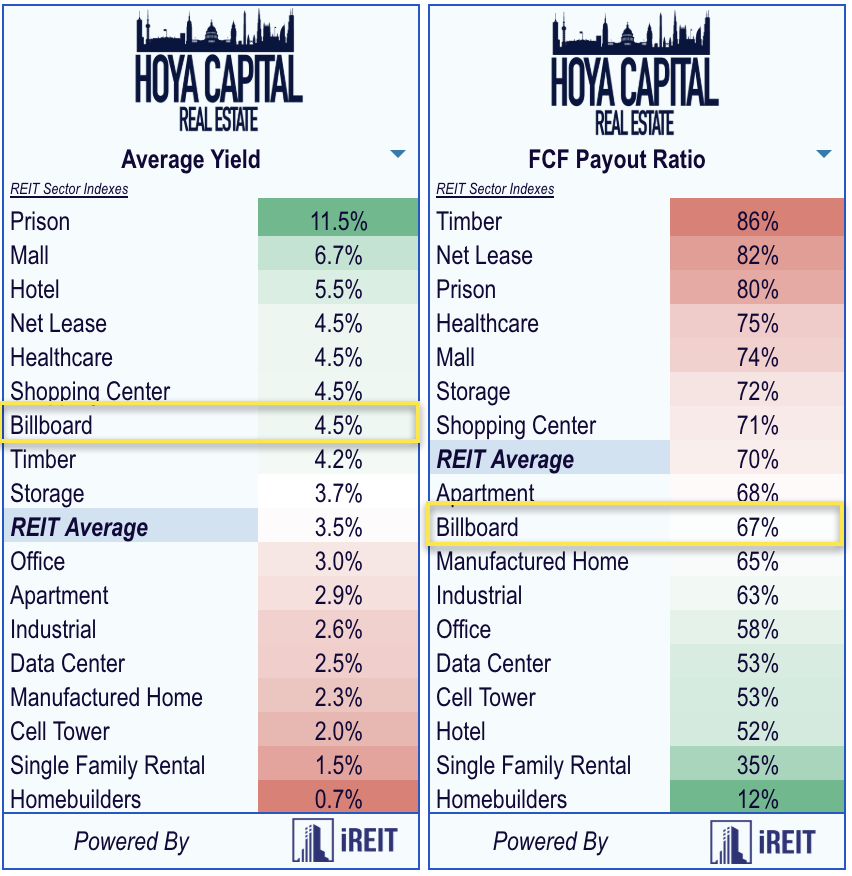

Billboard REITs are among the highest-yielding REIT sectors, paying an average dividend yield of 4.5% compared to the REIT sector average of 3.5%. Lamar is currently yielding 4.3% while Outfront is yielding 5.1%. Billboard REITs pay out roughly 70% of their available cash flow, leaving sufficient cash flow to fund the digital conversion upgrades and acquisition-based external growth. Our research finds that REITs with consistently lower payout ratios, on average, tend to outperform REITs that pay out a higher percentage of free cash flow.

Billboard REITs exhibit classic “growth-REIT” characteristics. These REITs are among the least interest-rate-sensitive REIT sectors, second-only to the hotel REIT sector, as measured by the Beta relative to the 10-Year Treasury Yield. Due to the high degree of operating leverage, these REITs are among the most economically-sensitive real estate sectors, again ranking just below the hotel REIT sector. We believe that billboard REITs are appropriate to counterbalance an otherwise interest-rate sensitive high-yield real estate portfolio, adding some economic-sensitivity and growth potential without sacrificing dividend yield.

Our Conclusions: An Attractive Under-The-Radar Play

As real estate investors, the phrase “significant regulatory barriers to entry” is like music to our ears, and it’s hard to dislike a sector enjoying steady “GDP-plus” demand growth with near-zero supply growth anywhere on the horizon. One doesn’t have to fully buy in to the hype surrounding the digital display conversions or cell-site leasing potential to see value in billboard REITs, which have a unique, growth-oriented return profile within the real estate sector while still paying a hearty dividend and offering attractive valuations.

At first glance, it’s easy to draw comparisons from billboard REITs to the high-flying cell tower REIT sector, one of our longtime favorites, which has similarly high barriers to entry and a high degree of industry concentration. Upon closer examination, however, it becomes clear that the billboard REIT business model and return profile are quite different, but that’s not necessarily a bad thing. Billboard REITs are one of the more operationally-intensive REIT sectors due to their large, labor-intensive advertising sales force, giving these companies inherent operating leverage. In that way, we see billboard REITs as more “hotel-REIT-like” in their return profile, exhibiting low interest-rate-sensitivity and being well-positioned to outperform if the US economy continues to chug along. Be conservative in an allocation, however, as advertising is the first line-item to be cut when times get tough.

Disclosure: I/we have no positions in any stocks mentioned, and no plans to initiate any positions within the next 72 hours. I wrote this article myself, and it expresses my own opinions. I am not receiving compensation for it (other than from Seeking Alpha). I have no business relationship with any company whose stock is mentioned in this article.

Additional disclosure: Hoya Capital Real Estate advises an ETF. In addition to the long positions listed below, Hoya Capital is long all components in the Hoya Capital Housing 100 Index. Real Estate and Housing Index definitions and holdings are available at HoyaCapital.com.

It is not possible to invest directly in an index. Index performance cited in this commentary does not reflect the performance of any fund or other account managed or serviced by Hoya Capital Real Estate. All commentary published by Hoya Capital Real Estate is available free of charge and is for informational purposes only and is not intended as investment advice. Data quoted represents past performance, which is no guarantee of future results. Information presented is believed to be factual and up-to-date, but we do not guarantee its accuracy.

- Advertisement -